Snowflake (SNOW) announced Q1 FY2023 earnings on May 25th. I will share a short summary of my reactions to the report, structured around positives, negatives and additional data points that are of interest. Overall, this report delivered a mixed bag, following a similarly obfuscated report in Q4. For investors, the challenge is to reconcile headline metrics with the underlying health of the business. Platform optimizations and the impact of customer macro concerns on a consumption business make this challenging in the near term. With explanations from management, these data points can be rationalized, but rely on faith in the long-term durability of Snowflake’s growth model.

Audio Version

View all Podcast Episodes and Subscribe

Let’s take a look at what happened and where the investment thesis lies. I won’t rehash all of the metrics, as those are readily available online in the earnings report and Investor Presentation. Additionally, Snowflake has a major customer event coming up from June 13 – 16, called Snowflake Summit. As part of this event, Snowflake will hold an Investor Day. This should provide an update on leadership’s longer term view of the business and overall product strategy. Information coming out of these events could represent a catalyst for the stock. For more background on Snowflake’s business, product offerings and competitive positioning, see my deep dives from past blog posts.

The Good

I think the highlight of the report focused on the rapid improvement in adjusted free cash flow (FCF). For Q1 FY2023, Snowflake delivered $181.4M of adjusted FCF for a margin of 43%. This is up significantly year/year from $23.4M and 10% adjusted FCF margin in Q1 FY2022. That represents a nearly 8x improvement in FCF and over 4x improvement in margin. On a GAAP basis, the improvement in net cash provided by operating activities was about the same as adjusted FCF.

With this trajectory, the leadership team updated their long term model for FY29 that was issued with Investor Day a year ago. They raised the target for adjusted FCF from 15% to 25% and for Non-GAAP operating margin from 10% to 20%. Investors may recall that analysts reacted unfavorably to the initial FCF target of 15% set last year. Raising to 25% just a year later was well received. Given this momentum and comparisons to peers (DDOG, CRWD), I think even 30% would be a reasonable forward assumption.

For the full year, they are targeting 16% adjusted FCF margin, raised a point from the initial estimate issued with Q4 earnings. Operating margin remained the same at 1% and gross margin at 74.5%. Going back three years, we can see the rapid improvement in these profitability measures. I think investors sometimes overlook the trajectory, by focusing on the most recent snapshot of values.

Operating margin improved as well. Non-GAAP Operating income for Q1 was $1.7M for an operating margin of about break-even. A year ago, non-GAAP operating income was ($35.8M) for an operating margin of -16%. That represents a significant swing in a year. Even on a GAAP basis, the operating margin improved from -90% to -45%. While still significantly negative, we can see the trajectory.

Net Revenue Retention

One of the most compelling parts of Snowflake’s unit economics is their phenomenal expansion rate. This is measured as Dollar-based Net Revenue Retention Rate. For Q1, this was 174%. In short, the Net Revenue Retention Rate (NRR), compares the product revenue for a cohort of customers in the prior 12 months to the same cohort during the year before that. At an NRR of 174%, customers on average increased their spend by 74% on Snowflake in the last 12 months. This would have a significant influence of revenue growth.

An NRR at these levels is unprecedented and not sustainable over time. Leadership has indicated that they expect the rate to decrease from here. Based on commentary included in Q4’s results, leadership expects NRR to stay above 150% for FY 2023 (this calendar year). This quarter, the CFO added that he expects “it will remain well above 130% for a very long time.” That would put Snowflake on par with other software infrastructure providers, like Datadog, with a best in class NRR.

As an aside, some analysts have interpreted this succession of NRR comments as a reduction quarter/quarter. Reading the earnings transcripts, my interpretation is that 150% applies to this calendar year, as it was said in conjunction with the initial estimates for FY2023. The 130% projection for a long time aligns with a similar statement made in August 2021 with the Q2 FY2022 results. Referring to NRR, the CFO stated “that number will come down, but I still think it will be well above 130, 140 for a very long time.” So, the change is the inclusion of 140% a year ago, which in context I don’t interpret as a significant change.

Another positive is Snowflake’s $5B in cash and equivalents with no debt. Given their existing cash and strong generation going forward, there is little concern that Snowflake will need to raise money by issuing more shares. This cash does provide an opportunity to pursue acquisitions, given the macro environment. While valuations of high growth public companies have been hurt, the same forces are lowering the cost of potential acquisitions. These could help Snowflake quickly add new technology capabilities (like Streamlit) and specialized staff. Some acquisitions may contribute to revenue as well. On the earnings call, the leadership team mentioned that they see acquisitions as an opportunity in this environment.

Data Ecosystem

Snowflake is demonstrating strong growth in data sharing activity. In Q1, the number of stable edges grew by 122% y/y. At this point, 20% of customers have at least one stable edge, up from 15% a year ago and 18% last quarter. Taking total customers into account for the year/year comparison, 1264 customers had at least one stable edge in Q1 FY2023, versus 680 a year ago. This represent 86% more customers with a stable edge year/year. The increase in customers using data sharing was 18% quarter/quarter. This growth underscores the importance of data sharing for customers, as paid use of the capability is required in order to be counted.

As investors will recall a stable edge represents an active data sharing relationship between two customers, where utilization credits are being consumed regularly to keep the data updated. Facilitating these data sharing relationships represent a competitive advantage for Snowflake, in my view. They increase customer retention, generate network effects to attract new customers and drive incremental utilization as shared data sets are filtered, cleansed and combined with other third party data. This network of data sharing relationships elevates Snowflake’s value proposition for customers onto a higher plane beyond focusing on tooling for analytics and ML/AI workloads within a single company.

Snowflake can offer a robust solution for those internal company needs, but is also providing the connectivity and capabilities to enable data flows and enrichment across industry ecosystems. I think analysts miss this point as they compare features side-by-side between Snowflake and popular alternatives. If the features for individual company analytics are comparable, then the value of the data sharing network should result in more competitive wins for Snowflake and higher retention. In addition, utilization to generate insights from combining data with other parties would represent incremental workloads beyond analytics processing for internal company reporting.

To enable data sharing and enrichment, Snowflake’s Data Marketplace provides users like business analysts with access to relevant data sets from third-party data providers. Companies can subscribe to these data sets for a fee and then seamlessly combine them with their Snowflake instance through data sharing. This eliminates the overhead of setting up separate integration processes to import, filter and combine this data. Additionally, secure data sharing handles updates automatically. That represents a huge cost savings. At the end of January (Q4), Snowflake had 1,100 data sets from 240 providers. For Q1 FY2023, listings grew 22% q/q to 1,350 data sets from over 260 providers. Data providers must find value in this relationship, as FactSet is buying Google Ads to promote their data set.

If the Data Marketplace is seeing strong growth, the Snowflake Powered By program seems to be garnering even more participation. This represents companies that have decided to build their data-driven product or service on top of Snowflake’s platform. For Q1, Snowflake announced there are now 425 Powered by Snowflake partners, representing 48% growth over the prior quarter’s count of 285. That is quite a jump. As these companies grow their businesses, their consumption of Snowflake resources should increase significantly.

At the same time, we have to acknowledge that some of the Powered By partners are start-ups themselves. Their rapid growth in 2021 likely fueled some of Snowflake’s outperformance last year as well. The shift this year in the macro environment could also be contributing to some of Snowflake’s recent consumption headwinds, as Powered By partner Lacework recently announced lay-offs.

Areas for Concern

Revenue Growth

My initial reaction to reported revenue was disappointment with the size of the Q1 beat and the limited raise for Q2 and the full year. Specifically, the company had set guidance for about 80% growth at the midpoint for product revenue in Q1 and delivered 84%. The magnitude of the absolute beat on product revenue was about $9M. This compares to the 7% beat in Q4 or $12M in absolute numbers, which was also soft.

Looking forward to Q2 (July end), product revenue guidance projects growth of 71-73% annually and 10.9% sequentially. These annual growth rates just met analyst projections. A similar sized beat in Q2 would bring annual revenue growth into the upper 70% range. This would represent another sizable deceleration from the prior quarter. The full year picture implies further deceleration. Leadership raised the bottom end of the product revenue target range by just $5M, leaving the annualized growth rate at 65-67%.

Management attributed this impact to a handful of consumer Internet companies that had grown their usage significantly last year, but have cut back consumption this year due to “shifting economic circumstances” which are unique to their businesses. Based on feedback from other sources, these companies appear to be Coinbase and food delivery services like DoorDash and Instacart.

Last year, we saw certain customers experience much higher than expected consumption — own businesses were growing extremely fast. Today, some customers face a more challenging operating environment. Specific customers consume less than we anticipated amid shifting economic circumstances, we believe are unique to their businesses, most notably consumer facing cloud companies. Although these customers are still growing, we believe as long as they are impacted by macroeconomic headwinds their consumption will be impacted.

Snowflake Q1 FY2023 Earnings Call, May 25, 2022

This certainly highlights one of the risks of a consumption based model, exacerbated by a portion of spend tied to human-driven, ad hoc activity. While these companies have commitments in place for a target spend over a longer time period, it would be easy to defer or slow down utilization quickly to reduce costs in the near term. This is likely what happened, as about 30% of activity on Snowflake is performed by data analysts running single investigations or projects, versus the other 70% of activity generated by repeating, automated jobs.

The CFO shared that this reduction was most pronounced week over week in April, but that the first few weeks of May saw improvement. This would explain the softness in Q1 and some conservatism in raising guidance going forward. Of course, in the same way that this activity was reduced, it could be just as easily added again, once these companies feel the macro environment is more stable. The consumption model cuts both ways.

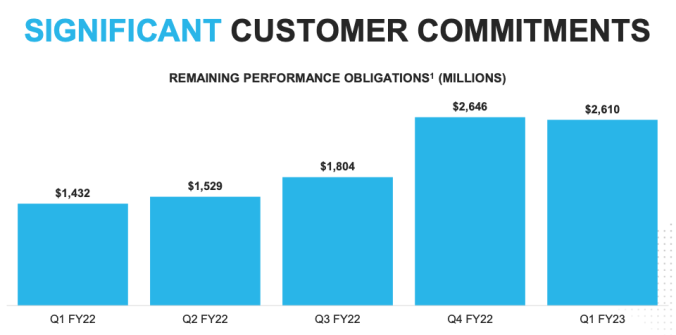

RPO in Q1 FY2023 was $2.6B, up 82% y/y, but sequentially slightly below Q4. That could represent a cause for concern, as the implication is that new sales commitments are slowing down significantly. Management pointed to the enormous jump in RPO growth sequentially in Q4 FY2022, which increased 47% q/q. They also highlighted their internal bookings number for Q1, which they said surpassed their target. Comparing to a year ago, RPO jumped about 44% from Q3 to Q4 FY2021, but only increased 7% from Q4 to Q1 FY2022. So, Snowflake performed slightly better in Q4 this year, but slightly worse in Q1.

Current RPO represents 53% of total RPO, and is up 79% y/y. This implies that $1.38B of RPO is expected to be consumed in the next 12 months.

Customer Activity

Snowflake added the fewest number of total customers in Q1 FY2023, compared to the prior four quarters. While the year/year growth rate of 40% is healthy (combined with high NRR), that growth rate has been decreasing. The sequential rate of customer growth dropped significantly in the year ago period from Q4 FY2021 to Q1 FY2022 as well, so this effect may be seasonal. The key will be to see where sequential growth lands for Q2 and Q3, as that will determine the trendline for this year.

Over the course of FY2022, we saw the sequential rate of customer growth stabilize in the 9-10% range for all four quarters. While the annual growth rate came down each quarter, this sequential rate would keep the annual rate above 40% going forward. If the sequential growth rate drops into the 6-8% range for FY2023 (current year), then the annual rate will drift down to 30%. Combined with NRR well above 130%, overall revenue growth can still remain above 50% with these customer growth numbers.

We will want to watch for any further deterioration. The demand environment narrative could be magnifying the effect in customer additions for Q1. Some companies on a legacy solution might be inclined to delay the start of their cloud migration.

Looking to large customer growth, we see similar trends for Q1, but continued strength at a high spending level. Snowflake had 22 more customers transition into the $1M+ tier in product revenue. This was up 12% sequentially, after a couple of quarters where this increased sequentially in the 20% range. We will want to watch growth in this area as well. Large customers contribute the majority of Snowflake’s product revenue and generate an outsized portion of NRR.

We do see evidence of continued spend growth at very high levels. In the earnings call, management reported that 10 customers crossed the $5M+ spending level (over trailing 12 months), bringing the total to 40 (33% sequential growth). They also reported having 10 customers above $10M in spend. For new sales, they reported booking four 8-figure ($10M+) deals in Q1, which was up from two of this size a year ago.

Interestingly, five of their top 10 customers’ product revenue grew faster y/y than product revenue overall (84% growth) . This influence of large customers also underscores the impact of the pullback in spend by the few highlighted consumer Internet companies. Management implied these fall into the large customer bucket.

The growth rate of those 5 large customers above 84% y/y is a staggering statement relative to the elasticity of spend. We can assume the top 10 customers are also those 10 who are above $10M in spend. For five of them to increase their consumption at that level at a rate higher than 84% is unusual in IT spending categories. Normally, companies slow down their rate of spend increase past some large amount, like $1M – $5M a year. To see companies spending over $10M a year increase their spend further at that high rate implies that the saturation level is much higher and highlights how large the addressable market is for this category.

Customer Verticals

New product categories seem to be contributing to growth as well, signaling that Snowflake’s alignment around industry verticals is bearing fruit. For Q1, they reported that product revenue from customers in their healthcare and life sciences vertical grew more than 100% year/year. Further, product revenue from customers in financial services grew just under 100%. Snowflake has created 6 other industry verticals in addition to these two.

For each, they bring together data providers, partners and contributors along the value chain. Then, they provide industry specific solutions to facilitate secure data sharing and workflows between companies. These efforts should drive network effects within each industry, as it becomes more efficient for each new provider to plug into the Snowflake ecosystem.

In March 2022, Snowflake formally announced the Healthcare and Life Sciences Data Cloud. This data cloud will allow organizations to securely aggregate, process and share data between participants. Snowflake protects sensitive data, allowing companies to meet compliance requirements and industry regulations. The goal is to help providers improve patient outcomes, optimize healthcare delivery and accelerate clinical research. Initial participants include Snowflake customers Anthem, Health Catalyst, IQVIA, Komodo Health, Novartis, and Spectrum Health.

The graphic above shows the data sharing relationships between participants in the Healthcare and Life Sciences vertical, shared as part of the announcement for the new vertical data cloud. Each point represents a company and the blue lines represent a stable data sharing edge. Assembling these data sharing relationships between participants in industry verticals may become a driver of continued Snowflake consumption in the future.

Other Data Points

I will be very interested to get further insight into Snowflake’s product roadmap. The upcoming Summit event in mid-June promises that. Snowflake’s CEO mentioned on the earnings call that “our summit conference in June will feature our most significant product announcements in four years.” I am generally a sucker for product innovation and that statement certainly grabbed my attention.

Putting the potential product announcements aside, the content of Summit will span 4 days with over 250 individual sessions presented by a combination of Snowflake employees, outside partners and customers. To gain an appreciation for Snowflake’s reach and penetration, one can peruse the extensive speaker list. While over half are Snowflake employees, the rest are customers and partners. The speaker list is sorted alphabetically by first name. Just the A’s span 48 people, including data leaders from BlackRock, JP Morgan, Adobe, Constellation Brands, Freddie Mac, Luma Health, Goldman Sachs, Disney, Capital One, JetBlue, Warner Brothers and Credit Suisse.

This speaks to the quality of customers that Snowflake is landing. The decrease in total customer additions is worth watching, as I noted. At the same time, Snowflake is focusing their sales efforts on those customers they think will drive $1M+ in annual spend. Also, notable is that once customers land on Snowflake, they tend to remain on the platform and continue to increase their spend. This is one software infrastructure business where churn is very low.

I’m sure there’s going to be some customers that are going to underperform. But likewise, there’s going to be many customers that overperform. And long-term, none of these customers are moving off of Snowflake and most have plans to do more with Snowflake.

Snowflake Q1 Fy2023 Earnings CAll

With Snowflake’s strong foundation in data storage and building ecosystems for data sharing, the product roadmap could go in several directions. Here are some thoughts:

- Commentary from the earning call implied a good portion of innovation will represent a doubling down on enabling developers to build data-rich applications on top of Snowflake. This development was accelerated by the Streamlit acquisition, which also closed in the quarter. I think this is an obvious extension. Currently, engineering teams need to copy data into another database in order to provide the back-end for a user-facing Internet application that is data rich. Allowing the application runtime to be pointed directly to a Snowflake instance provides a replacement for this data workload and eliminates the piping of data between the two sources. The simple outcome would be more utilization of Snowflake by shifting spend away from the other data source. Of course, this would only be appropriate for applications with a heavy read query pattern – it wouldn’t handle writes.

- Along the same lines, we could see additional capabilities added in and around Snowpark. A big part of Snowflake’s strategy is to allow companies to accomplish more of their analytics and even light ML work by keeping data within Snowflake.

- The Powered By program could represent a large opportunity for Snowflake, because they have whole businesses building a data layer on top of Snowflake, rather than reconstructing it from scratch on cloud infrastructure. This makes Snowflake core to their whole business, versus just enabling analytics processing. Additional capabilities to extend the reach of Powered By would be interesting.

- Finally, in addition to unlocking analytics within a company, Snowflake aspires to facilitate collaboration across industries. This is the context behind their label of the Data Cloud. Some analysts are predicting the next evolution of generalized cloud infrastructure representing layers of compute, network and data on top of core hyperscaler infrastructure. They are calling these “superclouds”. Snowflake could become the supercloud for data exchange. This article from Silicon Angle provides general context and conjecture for Snowflake’s potential role.

Hiring

Q1 was record hiring quarter. For the full year, Snowflake plans to add more than 1,500 net new employees. Most notable was the acceleration in sales and marketing hiring over the last two quarters. For Q1, Snowflake onboarded 19% more sales people over the prior quarter. This implies the company is not cutting back on growth investments as a result of fears over the demand environment. I also like that S&M and R&D are getting the majority of new hires.

Take-aways and Investment Plan

The Q1 earnings report was mixed. After sorting through the implications of platform optimizations from Q4’s report, investors now have to interpret the macro impact on Snowflake’s consumption model. This is the second quarter in a row in which Snowflake leadership had to craft creative explanations for tempered revenue growth. Bulls consider these rationale explanations that don’t signal deterioration of the business. Bears interpret these as signals of an inherent demand slowdown, increased competition or commoditization of the business.

This dilemma makes it harder to project an investment path forward. It’s easy to dilute concerns over the near term headwinds with faith in the long term potential of Snowflake’s addressable market, product positioning and leadership. Investors with a pure by-the-numbers approach are probably justified in cutting their losses (as we recently touched a 52 week low). A more optimistic view assumes that 2022 will be bumpy for Snowflake, but stabilization in the macro environment looking forward will remove these headwinds and allow Snowflake to sustain a high level of revenue growth for many years. Combined with a refreshed view of Snowflake’s ability to generate meaningful free cash flow, Snowflake could quickly grow past valuation concerns through compounding.

Revenue deceleration always looks concerning for investors, as they project the same rate of deceleration going forward. We have seen this effect before as some hypergrowth companies rapidly decreased revenue growth by 5-10% per quarter from 80%+ annually. Eventually, they stabilized at a steady state. In some cases, that was 20-30% over a short period. For others, the companies appear capable of maintaining 50-60% annual growth, for at least the near future. While investor sentiment can be negative during the reduction phase, as the growth rate stabilizes, confidence returns.

Crowdstrike (CRWD) provides a good example of this effect, as they rapidly dropped from 86% revenue growth in Q3 FY2021 to 63% in Q3 FY2022 (reported in Dec 2021). Investor sentiment dampened during this period. When Crowdstrike delivered 63% growth again for Q4 FY2022 (March 9, 2022), sentiment improved substantially. This was reinforced by forward guidance which implied that low 60% growth could be reached again with a similar beat. That inflection drove the stock up 12% the day after earnings.

I could see a similar outcome for Snowflake, when macro headwinds abate and companies cutting back consumption bring it back to contracted commitments. As companies have macro concerns, it is easy to reduce many of the ad-hoc, growth-oriented analytics queries (i.e. “give me a list of customers most likely to respond to this promotion” for an email campaign). Once those companies feel comfortable again, it will be just as easy to bring back that activity.

Further, while NRR will decrease from the 170% range, it is likely to remain “well above 130% for a long time.” Coupled with a reasonable rate of new customer additions, I can see a scenario where 50-60% annual revenue growth is sustainable. This will be further enhanced by any new product offerings, which management has stated were not factored into the FY2029 revenue projection of $10B. Similar to CRWD, as revenue growth rate settles into a sustainable, high rate, we could see a similar shift in sentiment. Valuation growth will start to be driven by the compounding forward of revenue and FCF.

What is becoming clear is that analysts and investors alike are shifting to appreciation for improvements to profitability on par with growth of revenue. The metric for profitability I see referenced the most is free cash flow. If valuations will be driven by multiples of free cash flow as much as multiples of revenue, then it’s fair to examine growth of FCF y/y as closely as we examine revenue growth. If a company can maintain a reasonably high revenue growth rate (let’s say 50% or more over time) and increase FCF faster, then they will likely benefit from dual tailwinds supporting valuation.

Since we are already half way through 2022, I think a good way to consider the potential for companies is to start looking forward to 2023. I am estimating that Snowflake finishes 2022 (FY 2023) with roughly $2.1B in total revenue. This represents a 70% y/y growth rate over FY 2022, and is down from my prior estimate for 80% growth. The factors contributing to the reduction are the performance optimization announced with Q4’s results and the impact of spend reduction from several customers due to the macro environment.

I think the impact of these factors will dissipate by 2023. Assuming that holds, then I project 60% revenue growth for next calendar year, bringing total revenue to $3.36B. I think that NRR can remain “well above” 130% and total customer growth can meet or beat 30% annually. These values for the same metrics mirror Datadog, which has been able to sustain revenue growth at these levels. Like Datadog, Snowflake is expanding their addressable workloads through product development as well, with Snowpark, data applications (Streamlit), the data marketplace / data sharing and the potential contribution of Powered By.

Similarly, I think adjusted FCF margin could surpass 20% next year, yielding at least $700M in FCF. This is based on the long term target for 25%, the current year target of 16% and the large improvement y/y we have been observing. A $700M FCF total in calendar year 2023 would represent about a 100% increase over the current year projection. This is based on a revenue estimate of $2.1B with a 16% FCF margin for $336M.

At a current EV of about $37B (from YCharts), we get forward multiples of:

- EV / Revenue = 37 / 3.36 = 11.0 (Growing revenue at 60% y/y)

- EV / FCF = 37 / 0.7 = 52.8 (Growing at 100% y/y)

If these trends in revenue and FCF growth materialize in early 2023, I think investors will be willing to pay 30-50% more for the stock. Of course, the risks to this thesis are that Snowflake growth slows down further or that the market conditions deteriorate beyond the valuation compression that we have already experienced.

I can’t predict the macro environment. Regarding Snowflake’s growth, my view is that the rapid revenue growth deceleration we are experiencing this year will stabilize into the 50-60% range for several years forward. The large market opportunity in data, Snowflake’s independent position with the hyperscalers, the potential for new product offerings and ongoing customer expansion all give me confidence for this. Once the market appreciates that growth of 50-60% is possible and FCF generation ramps up, then I think we will see the valuation multiple stabilize. Revenue and FCF growth will then influence the stock price proportionally and compound going forward.

For my portfolio, I have brought my allocation down to 18% for SNOW. While I am still bullish about the prospects as I have laid them out, the last two quarters of performance has introduced some execution risk. If Snowflake’s progress over the remainder of 2022 shows evidence of improvement going into 2023, I may slowly increase the allocation again. In the meantime, I added funds to DDOG and NET, which now represent the two largest positions in my portfolio.

Further Reading

- Peer analyst Muji over at Hhhypergrowth published a detailed update on Snowflake. This included recent earnings, as well as a number of product announcements. His analysis is always thorough and represents a great supplement to mine. Check out his latest post. If you aren’t a subscriber, you should seriously consider it.

NOTE: This article does not represent investment advice and is solely the author’s opinion for managing his own investment portfolio. Readers are expected to perform their own due diligence before making investment decisions. Please see the Disclaimer for more detail.

Service now has been trading at an avg P/S of 15 times. At 3.3B revenue, we can expect snowflake to reach 50B marketcap i.e 165 a share. And then we can expect the share price to grow at Sales or FCF growth rate i.e 50% , minus the share dilution.

I think this is inline to what you have projected as well.

This gets to a 2024 target of around $350 at max.

What are your thoughts on the 2024 target now?

Yes. I am targeting $5B in revenue for 2024 (FY 2025) at this point. That would represent 50% growth over my updated revenue target of $3.36B for 2023 (FY 2024). I also think that FCF could reach 25% by that time, representing $1.25B in FCF. Servicenow revenue growth was 27% in the most recent quarter with 31% trailing FCF margin. That revenue growth rate might be a little low for a valuation comparable. A 20 P/S multiple is probably justified for 50% growth with high cash flow. That implies market cap of $100B, or about 2.5 current value. So, a revised stock target of $325 (agree $350 max) in 2.5 years.

Of course, determining the valuation multiple to use is the key input.

Regarding the consumption charges changes mentioned in q4, don’t you see a revenue impact due to that ?

Yes – those were taken into account when management initial projected the FY 2023 growth rate of 65-67%. I think investors and analysts (myself included) were assuming that was a conservative first pass and they would gradually raise that growth rate each quarter. When they didn’t raise the full year guide in Q1, the reason was the impact of consumption reductions by a few customers. Without the platform optimizations this year, we could give Snowflake credit for about $100M in addition revenue, if we wanted to compare FY2022 to FY2023 on an apples-to-apples basis.

Anybody who knows me, Peter, knows I read a lot. I often liken myself to a whale swimming the oceans, maw open as I go along, swallowing krill whole. But when it comes to your commentaries, I slow my pace accordingly and read (ingest) slowly. That slowed pace is amply rewarded because you dish up sapid bites such as…

01. “This certainly highlights one of the risks of a consumption based model, exacerbated by a portion of spend tied to human-driven, ad hoc activity. While these companies have commitments in place for a target spend over a longer time period, it would be easy to defer or slow down utilization quickly to reduce costs in the near term.”

You dig beneath the headline numbers and find insight. Armed with that insight, investors know what to watch for in future reports.

02. “Snowflake added the fewest number of total customers in Q1 FY2023, compared to the prior four quarters.”

Again, you provide insight. If a growth company can be simply explained as a company with growing revenues, growing earnings, and a growing list of customers… then what happens to the future revenues and earnings if the growth of customers stalls? Sure the headline numbers will be better but their velocity will be comparatively negative; an early warning sign. As you note, an item to watch.

03. “This is the second quarter in a row in which Snowflake leadership had to craft creative explanations for tempered revenue growth.”

Ouch! 🙂

04. “Revenue deceleration always looks concerning for investors, as they project the same rate of deceleration going forward.”

You note one problem (a company’s cadence of growth), but a second problem for investors is how to value that slower cadence of growth. So while Snowflake’s revenues and earnings might get… lumpy, SNOW shares likely will get bumpy as investors attempt to discover the correct valuation metrics and their ranges to accord with the changing (slowing) pace of growth.

05. “I have brought my allocation down to 18%…”

Any reader who has read this far might have gasped. I did. Has there been a bigger bull on Snowflake’s prospects than you and SSI? (Perhaps Matthew.) You note you will watch Snowflake for a return of its growth cadence and in lockstep scale up your position – but the obverse is equally possible, that growth continues to slacken and you exit your position altogether. You gotta love investing! 🙂

06. “Snowflake formally announced the Healthcare and Life Sciences Data Cloud.”

Hmm. Is this a competing product to Veeva[‘s Vault]…?

Thank you for another helpful, insightful, and useful commentary.

me

Hi David – thanks for the feedback and highlighting relevant content. I agree that investing is a challenge both analytically and emotionally. I try to balance an objective measure of near term performance with my more subjective view of a company’s potential based on their product development cadence, market direction and the competitive landscape. If the numbers aren’t lining up to the potential, I have to make smaller adjustments, even when I am still bullish. I suppose that is more about portfolio management than single company analysis.

I am not that familiar with Veeva’s Vault, so can’t really provide insight there. Great to hear from you!

Thank you, Peter, for yet another great update, really appreciated!

Although I enjoy your posts a lot and there’s perhaps a little hope that the worst is past with these stocks I find myself a bit worried wrt overall situation with tech/saas companies and stocks. It looks like quarter after quarter the number of companies executing flawlessly is getting smaller and smaller and your current holdings reflect this to a certain degree, we’re more or less left with only two names without cracks as of today. And after the next ER round, who knows.

This is perhaps related keeping the bar very, very high but OTOH I think it’s also true that as quarters go by we have fewer and fewer those “perfect 10” tech/saas companies left to invest in. I’d be curious to know what are your thoughts around this? Do you perhaps see this changing going forward or causing some overall sentiment changes? CRWD you mentioned is definitely a positive example and showing that the first slowdown doesn’t automatically warrant excluding the company from potential investment candidates but there are also quite a few companies that whipped to look great around IPO and haven’t been exceptional in any way since then.

Hi – thanks for the feedback. Unfortunately, I don’t have a good answer here. As you have seen, my portfolio is becoming increasingly concentrated around those software infrastructure companies that appear to be executing the most consistently. As we face macro headwinds and post-Covid growth normalization, it seems like fewer companies are exhibiting durable high growth. I am watching a few that may start to exhibit the potential for re-acceleration and improving operating margins. This could provide another company or two to add to the list.

Thanks for the update, I really appreciate your writing.

Is data mesh bad for Snowflake?

Hi Michael – not necessarily bad and actually could be good. Data mesh is an architectural pattern that enables individual teams within an enterprise to operate on their data sets independently, versus relying on a central data team to do everything for them. Data mesh doesn’t prescribe a specific technology implementation and aligns with Snowflake’s capabilities. Data mesh relies on four principles: domain ownership, data as product, self-serve infrastructure and federated governance. Snowflake can be used as the data management engine for this model. This web site provides a good overview and even cites Snowflake+dbt as a reference implementation: https://www.datamesh-architecture.com/.

Thanks!

Strangely, the link didn’t work, twice, until I found it through google, and now it does.

When I copy and paste it, I don’t get the “/” on the end:

https://www.datamesh-architecture.com

I also found:

dbt and Snowflake https://www.datamesh-architecture.com/tech-stacks/dbt-snowflake

In the piece on that site about “dbt and Snowflake”, I got as far as this,

“There are pre-built solutions to ingest Kafka messages, and it is quite common to use a managed service like Fivetran or Stitch to replicate data from databases or SaaS providers, such as Google Analytics or Salesforce.”

and I thought, replicating data seems expensive and inefficient if it isn’t used for a backup, so could there be a trend for opportunities like, a CRM provider (probably not Salesforce) having their data on Snowflake so customers using Snowflake don’t need to replicate it?

Thank you for another great insight!

I just want to add some color on how I look at SNOW’s growth. I feel it might be a little higher to project 60%+ growth in near term. I get the way you project it by combining 130%+ DBNER and 30%+ customer growth, and that’s exactly how I think of ‘future growth’ for most SaaS.

However, SNOW have a different model. With long sales cycle, SNOW’s future growth might be much more closer to DBNER(expand). For example, new customer counts for like 15% of DDOG’s revenue, while for SNOW it only counts 1%. Unless they manage to land bigger and faster, I don’t think ‘land’ part can contribute more to their ‘current growth’. SNOW’s growth should be driven mainly by ‘expand’, while ‘land’ is more about ‘future growth sustainability’.

Of course, I totally agree with you about SNOW’s future opportunities. This is just some modeling thoughts by an equity analyst. Once again thank you for the excellent analysis.